South Korea

- South Korea’s refining sector is a transmission belt for global supply disruptions. As a major exporter of refined fuels, petrochemicals, and jet fuel, disruption to Korea’s oil and feedstock imports flows through to higher transportation, aviation, and manufacturing costs that cut across industries globally.

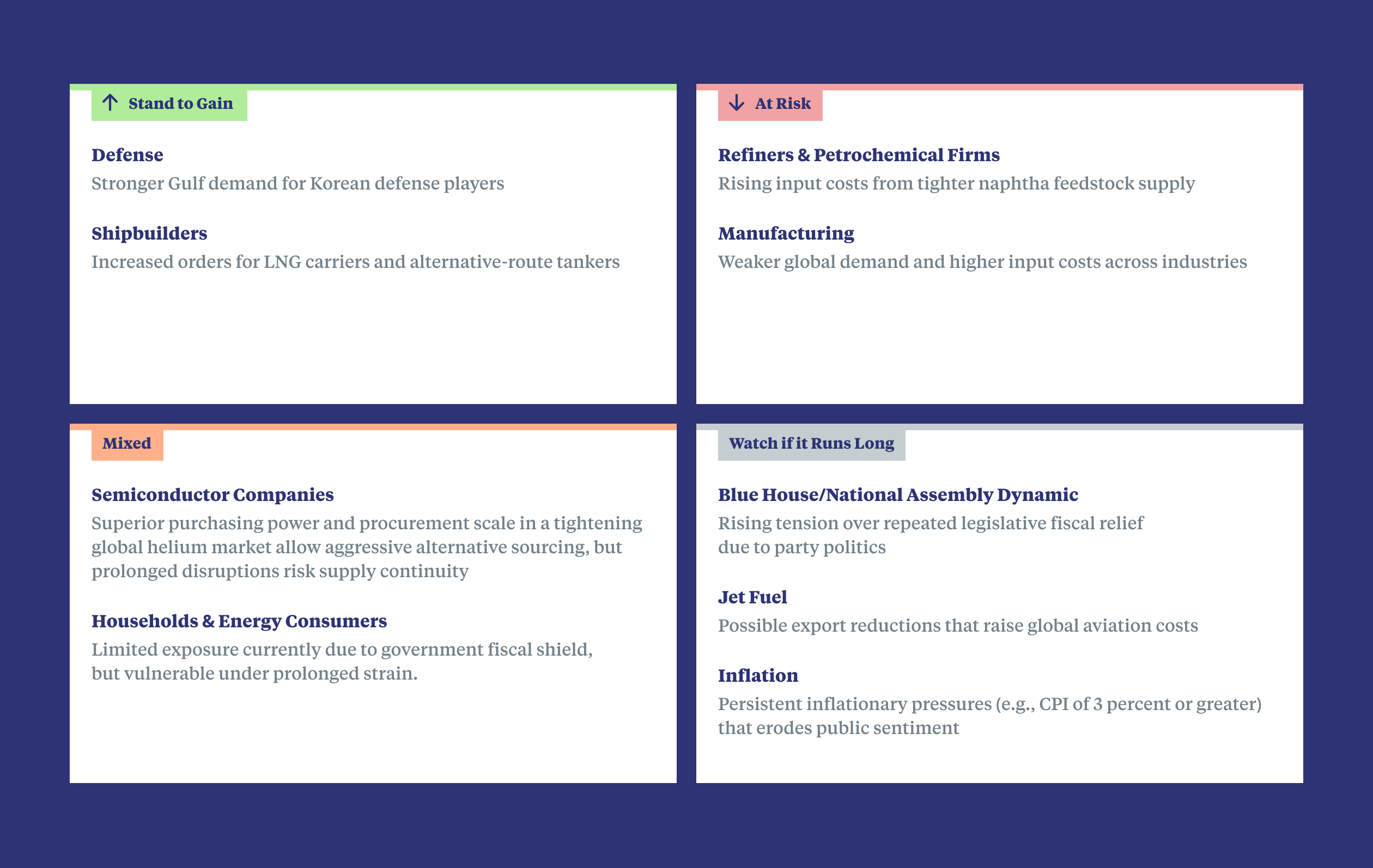

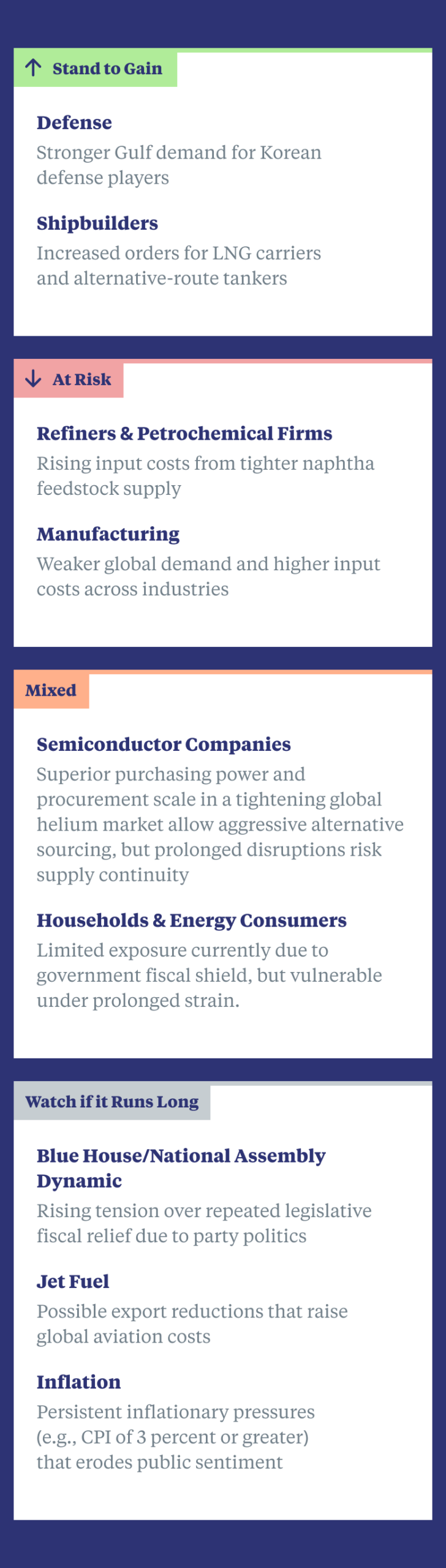

- South Korea’s chip industry has shielded the broader economy, but the crisis underscores the risks of overreliance. Amid energy and import shocks, Korea’s booming semiconductor industry is carrying much of the country’s economic growth. Korea’s chipmakers are themselves exposed to LNG prices and helium imports, 65 percent of which came from Qatar in 2025 — making extended Strait disruption a direct threat to Korea’s most important growth engine.

- Political fallout will depend on whether rising prices are seen as fairly distributed. The Hormuz disruption has become a political test for South Korea, centered on how costs are shared across government, households, utilities, and strategic industries. The June 3 local election results were broadly seen as a loss for the ruling party, increasing pressure on the Lee administration to manage the burden carefully.

- Economic and energy security will move to the center of South Korea’s strategic agenda. Strategically, the crisis deepens Korea’s energy reliance on the United States even as the broader bilateral relationship grows more complex. Seoul is doubling down on supply chain resilience, energy security, and closer coordination with partners such as Australia and Saudi Arabia but is also diversifying to Russia for key inputs, including helium. The conflict has accelerated South Korea’s warming with Japan, with relations improving to levels not seen in decades as the neighbors work together on energy security issues such as mutual supply and swap arrangements for oil and LNG.

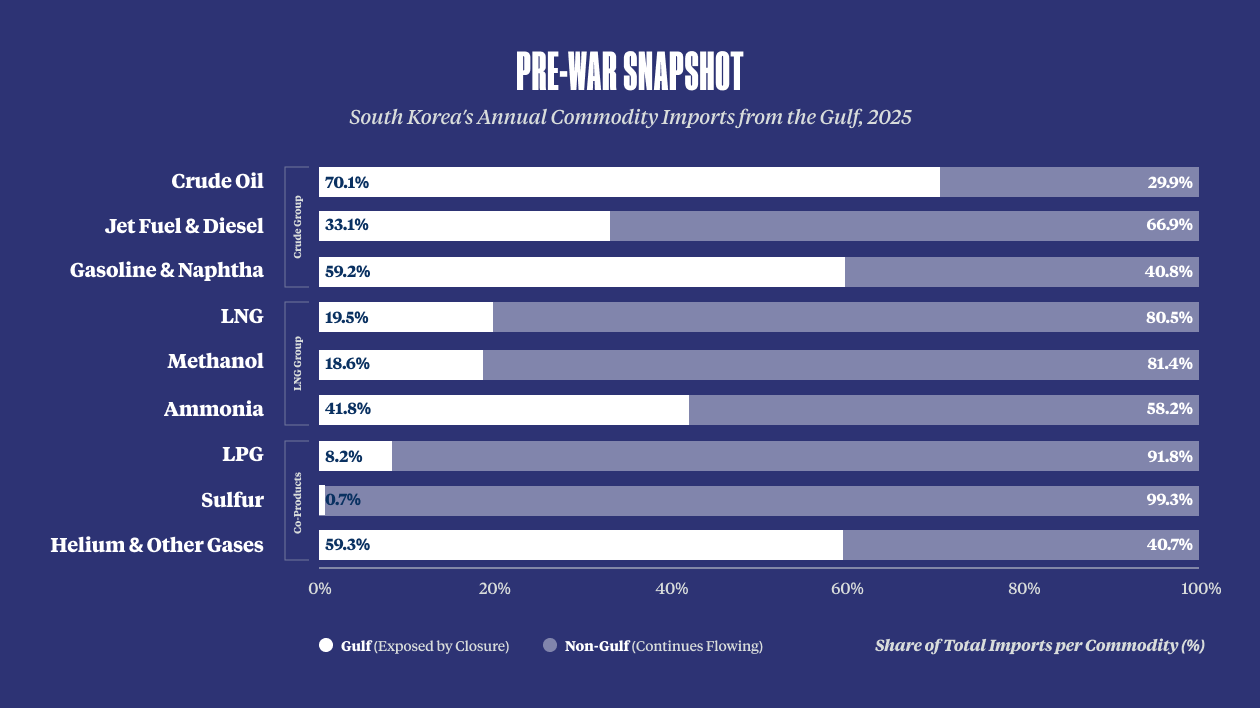

On the eve of the crisis in the Strait of Hormuz, roughly 70% of South Korea’s crude oil imports and a substantial share of its liquid natural gas (LNG) imports passed through the Strait of Hormuz, creating significant vulnerabilities for the country’s refineries and petrochemical plants. The risk also extended beyond energy: key high-tech industries, including semiconductor manufacturing, relied on Gulf-sourced inputs such as Qatari helium and other specialty gases.

Pre-War Snapshot

South Korea’s Annual Commodity Imports from the Gulf, 2025

Economic Impacts

Macroeconomic Picture

Timely government intervention, healthy inventories, and moderate seasonal energy demand have cushioned the impact of disruptions so far, but pressures are building under the surface. The trajectory of price increases, inventory drawdowns, and procurement conditions are key watchpoints. Higher import costs keep pressure on the won and could push inflation above the 2.5 percent baseline, limiting the Bank of Korea’s room to cut rates, eroding real incomes, and dampening both consumption and investment. Growth is projected to nearly double to 1.9 percent in 2026, but a sustained disruption could shave up to a full percentage point off this target.

Jet Fuel

South Korea is the world’s top jet fuel exporter by a wide margin, accounting for 30 percent of the global market and nearly 70 percent of U.S. imports. Sustained production cuts would raise costs for international shipping and travel, and because jet fuel prices feed directly into air freight rates, downstream effects would ripple through supply chains well beyond the aviation sector.

South Korea is the world’s top jet fuel exporter, accounting for 30 percent of the global market and 70 percent of U.S. imports

Petrochemicals

Korea’s petrochemical industry and petroleum refining sector are the world’s fourth and fifth largest, respectively, and feed global manufacturing supply chains for synthetics, electronics, autos, consumer goods, and other products. Both industries rely heavily on crude oil and naphtha from the Gulf. Korea’s refineries are optimized for Middle Eastern heavy crude, leaving them exposed to rising supply costs as the market reorients toward more expensive U.S. light crude. These pressures add to preexisting challenges for the sector, including Chinese overcapacity. Prior to the conflict, major firms were already undergoing restructuring and cutting production. New disruptions to crude and feedstock supplies that accelerate contractions in Korea’s petrochemical output will flow through global supply chains, deepen concentration and overcapacity risks, and undercut Korea’s competitiveness in industries Seoul is counting on to drive the next phase of growth, including EV batteries, semiconductors, and synthetic materials.

Semiconductors

South Korea’s semiconductor industry produces the leading-edge memory products underpinning the global AI boom. It relies on stable, low-cost electricity, petrochemical-derived inputs, and specialty gases: South Korean chip manufacturers are the world’s largest helium consumers and source over 65 percent of their supply from Qatar. Government intervention and aggressive diversification efforts, combined with leading firms’ willingness to pay premiums for inputs, have contained immediate supply challenges. But a prolonged disruption will force them to lock in expensive long-term contracts or divert R&D capital toward supply security — opportunity costs that compound over time for Korea’s flagship technology sector.

South Korea: Risks & Opportunities by Sector

Outlook

South Korea has managed the initial Hormuz shock through a combination of tools: strategic reserve releases, fuel tax cuts, price controls, refiner compensation, naphtha export restrictions, a war risk insurance backstop, and looser stockpiling rules. These measures can continue to buffer supply impacts through the early fall, but the costs are increasingly falling on households, utilities, refiners, and the fiscal balance. If disruptions persist through 2026, Seoul will likely seek a supplementary budget to extend relief and support key sectors. With the ruling party controlling both the executive and the National Assembly, the watchpoint is not whether new measures pass, but how quickly and at what scale. Criticism will come from two directions: opposition and fiscal hawks who frame household relief as populist spending, and progressive lawmakers scrutinizing refiner support.

A longer disruption would deepen a more fundamental vulnerability: Korea’s near-term resilience depends on a few sectors, especially semiconductors and petrochemicals, that in turn rely heavily on energy, feedstocks, and inputs from the Middle East. Semiconductor production cuts are still a low-probability tail risk even under sustained price pressure. Petrochemical volumes would tighten sooner, and any significant curtailment would make Korea a source of wider supply chain disruption. Key signals to watch are whether inventory drawdowns are replenished and whether procurement cycles reset at higher cost.

The decisive challenge for Seoul is not immediate shortages but how long it can sustain politically viable burden-sharing across households, utilities, refiners, and strategic industries without eroding public support or fiscal headroom

Fuel-control and fiscal decisions in late October, combined with the onset of winter demand in late November, will set the pace at which price pressures spread from energy into food, transportation, and manufactured goods — producing a mild stagflationary environment of slower growth, higher inflation, and compressed household incomes. Equally consequential will be the speed at which disrupted production is restored and the rate at which shipping lanes reopen and inventories are replenished, as delays in either will deepen and extend inflationary pressures across supply chains. Over time, the decisive challenge for Seoul is not immediate shortages but how long it can sustain politically viable burden-sharing across households, utilities, refiners, and strategic industries without eroding public support or fiscal headroom.