China

- China is emerging from the crisis with clear economic and strategic advantages. A shared global crisis has become a demonstration of China’s resilience, thanks to its large oil and gas reserves and diversified energy supply. Its ability to absorb and cushion the global energy shock is reinforcing China’s competitive edge across industries, while higher costs accelerate a shift to clean-tech sectors that China dominates. Economically and geopolitically, Beijing is using the crisis to promote China as the stable partner of choice.

- Even where pain points exist, Beijing is confident in its ability to manage them. China is not immune to prolonged disruptions, which would erode stockpiles, dampen already sluggish consumer demand, and squeeze industrial margins through higher energy and petrochemical input costs. But the question is how long China must cope, not whether it can. Beijing’s ability to set prices and export controls, deploy subsidies, and manage its currency gives it more shock absorbers than most. Beijing sees the crisis as the ultimate validation of its industrial self-reliance strategy: it will double down on, not deviate from, the current Five-Year Plan.

- The deeper risk for Beijing would be if prolonged disruptions slow global growth and dampen demand for Chinese exports. Higher energy prices through late 2026 would weaken global purchasing power, tighten financial conditions, and increase the risk of recession, particularly for commodity-importing emerging markets. The compounding effect would be to limit these markets’ ability to absorb Chinese exports, narrowing a key release valve for China’s export-driven economic model, which is already under pressure as the United States and Europe pursue trade barriers to counter Chinese overcapacity.

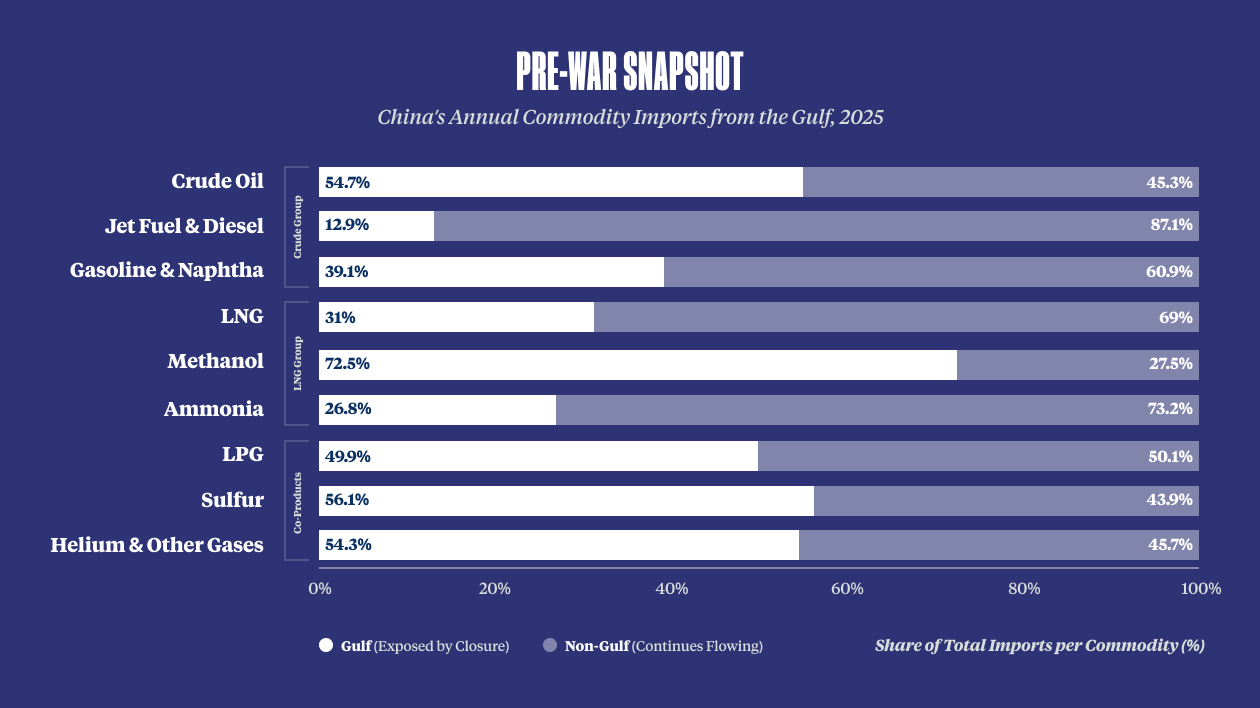

Prior to the breakout of the crisis, the Strait of Hormuz was an important conduit for China’s imported crude oil, helium, and petrochemicals, among other critical commodities. At the same time, China maintained a large crude oil reserve and has recently worked to reduce its overall imports and diversify energy suppliers.

Pre-War Snapshot

China’s Annual Commodity Imports from the Gulf, 2025

Economic impacts

Macroeconomic Picture

Higher oil prices and stronger dollar demand are putting renewed downward pressure on the Chinese yuan (RMB), complicating Beijing’s effort to keep the currency broadly stable while deflecting foreign criticism that an undervalued RMB is reinforcing China’s export overcapacity. With ample reserves and capital controls, this is a problem to be managed, not a crisis. Higher energy and freight costs are adding to household budget pressures that never fully recovered from COVID and China’s property market collapse. Inflation, even at manageable levels, directly challenges Beijing’s push to rebalance toward consumption-driven growth.

Crude Import Resilience

China has absorbed the crude shock less by fully replacing lost Gulf barrels than by reducing the need for imports overall, which it has done through a combination of modest inventory drawdowns, lower refinery runs, and other types of demand constraint. To conserve supply, Beijing imposed export restrictions and quotas for refined fuels and allowed refiners to reduce output rather than process expensive crude oil. At the same time, growing EV and renewables adoption, gas and coal substitution, greater rail utilization, and slowing construction activity have further softened gasoline and diesel consumption. China appears to have offset around a third of import flows lost by Hormuz disruptions via reroutes, pipelines, and new supplies — notably from Brazil — but the larger adjustment has come from importing less: China’s crude imports fell from 11.5 million barrels per day (bpd) in May 2025 to 7.8 million bpd in 2026.

Petrochemicals & Plastics

Strait of Hormuz disruptions have exposed the limits of China’s self-sufficiency in key inputs such as sulfur, chip-grade helium, and the Gulf-sourced naphtha that serves as a feedstock for the plastics, synthetic fibers, and chemicals that China supplies globally. The damage so far is concentrated among smaller independent refiners and petrochemical producers, showing up in reduced production, isolated force majeures, and missed orders, but over time would transmit across plastics, chemicals, and packaging sectors. Beijing has tools to respond, including price caps, export restrictions, and production mandates. These interventions can cushion feedstock constraints for 2-3 months, but a longer disruption would have downstream effects for global industries ranging from medical devices and pharmaceuticals to automotives and consumer electronics.

Semiconductors

Roughly 60 percent of China’s chip-grade helium is sourced directly from Qatar’s North Field, which was damaged early in the conflict. In the near term, leading Chinese chipmakers — like those in Taiwan, Korea, and the United States — will simply pay a premium to maintain production, with modest impact on margins. If price increases give way to outright helium shortages, China is comparatively well-placed to deploy state resources and geopolitical leverage to secure supply above market rates, including from Russia. Longer term, the shock may accelerate China’s domestic helium extraction investment, which cannot replace Gulf supply quickly but would reduce vulnerability and create additional supply chain leverage over time.

Renewables

Beijing has leveraged the Hormuz crisis to frame its renewables investment and exports of renewable technologies as strategic foresight. With 1.4 terawatts of operating renewable capacity already online and a reported 90-110 days of crude import cover in reserve, China weathered the initial shock better than any regional peer — and the crisis will further bolster China’s renewable energy, EV, and battery industries. Though China’s 15th Five-Year Plan already committed long-term support to support green technologies as part of its industrial upgrading agenda, the Hormuz disruption will further incentivize domestic adoption to reduce fuel import reliance.

China: Risks & Opportunities by Sector

Outlook

With Xi’s fourth term beginning in 2027, Beijing’s overriding priority is to project stable leadership. China’s ruling elite are acutely aware that the Hormuz closure’s economic effects, from higher energy and food costs to localized layoffs amid refinery cutbacks, land on top of already-stressed household finances and elevated youth unemployment. Geographically concentrated shocks in refinery towns carry real social risk. Beijing’s response will proceed in predictable stages: stockpile releases, Russian and overland supply substitution, price controls, targeted subsidies, and foreign exchange intervention — all to prioritize stability over market price-clearing.

China could use its estimated crude stockpile of 1.4 billion barrels to replace up to eight months of imports

If the ceasefire does not hold, Beijing would likely be able to manage another disruption of 3-6 months, but at a rising cost. With China’s estimated crude stocks around 1.4 billion barrels before the Hormuz disruption, it could hypothetically replace up to eight months of imports lost from inventories alone — and up to 12 months if it continues to replace one-third of lost imports through reroutes — assuming all stocks are operational. However, as stockpiles are finite, and Beijing prefers to maintain large buffers, its strategic calculus would likely shift in favor of further cost absorption and demand controls. Independent refiners and petrochemicals would face the most immediate pressure, with state refiners receiving priority over more export-oriented industries. The longer the disruption, the more China’s response would depend on its ability to cut refinery output, subsidize fuel costs, and suppress demand.

Ultimately Beijing views the pain points not as existential threats, but as challenges to be managed and even opportunities to be exploited. Domestically, the supply shock could accelerate long-sought structural reforms to enhance resilience by fast-tracking consumer-led growth and accelerating the push into renewables and nuclear energy. Economically, China will deepen ties with the Global South as diversification takes precedence over de-risking. Geopolitically, the crisis allows Beijing to cast the United States as the destabilizing actor whose Middle East entanglements impose costs on the world.

The crisis allows Beijing to cast the United States as the destabilizing actor whose Middle East entanglements impose costs on the world.

A more prolonged disruption would complicate Beijing’s efforts to reduce external dependencies and boost domestic consumption. Ultimately, however, short-term pain for industry and households would be outweighed by longer-term advantages that are accruing to China in key industries and relative to other major economies.

The strategic risk for Beijing is that higher energy prices through fall and winter could weaken global growth and even tip key markets into recession. For China, the effects would be felt as collapsing export orders — first from emerging markets in Southeast Asia, which are both manufacturing partners and export destinations, and then from advanced economies, particularly in Europe. In addition to squeezing Chinese exporters, slower global growth would set back Beijing’s plans for outbound investment in sectors such as EVs and batteries and could intensify the building political backlash against China’s trade policies.