Japan

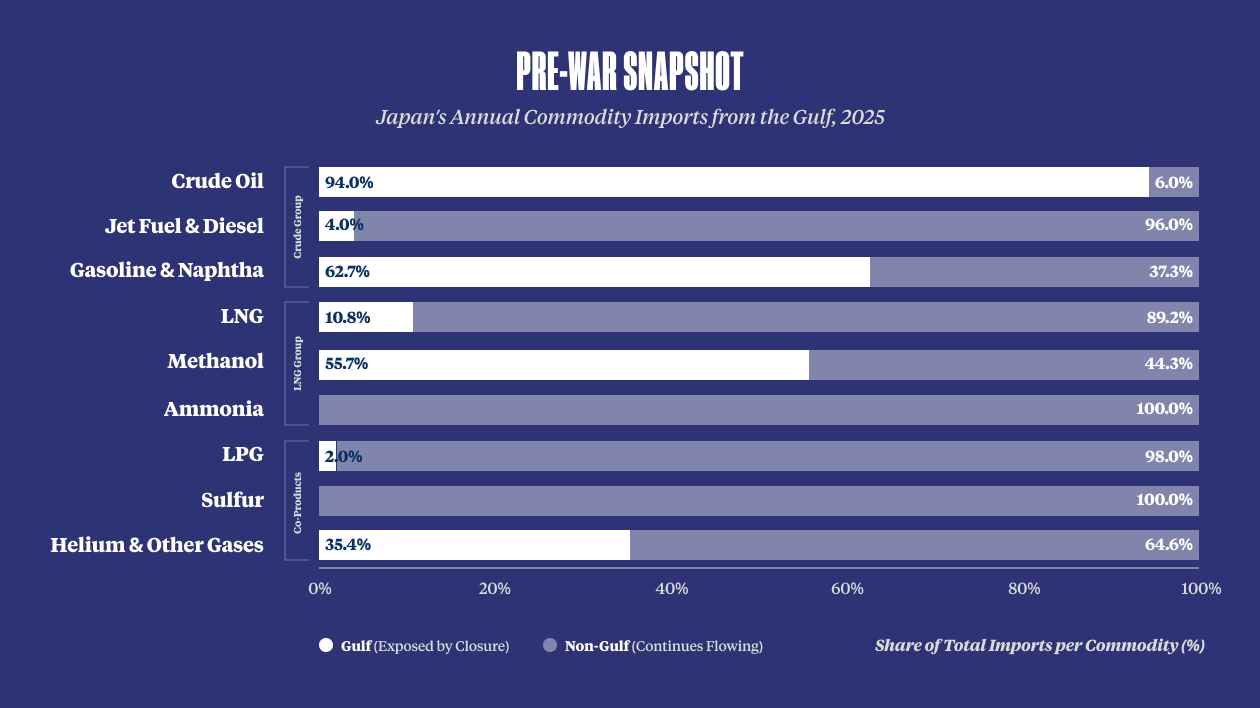

- Japan has weathered initial shocks but would face fiscal and financial stability risks from a protracted disruption of the Strait. Japan relies on the Gulf for roughly 95 percent of crude imports but has so far managed disruptions thanks to reserves that can cover demand well into 2027. Sustained higher energy prices would cause fiscal pressures to compound quickly: fuel subsidies to date are equivalent to half the defense budget, bond yields are at 30-year highs, and debt servicing already consumes a quarter of the national budget, leaving Prime Minister Takaichi with little room to maneuver in addressing Japan’s intertwined fiscal, defense, and stagflation challenges.

- Rising fiscal pressures have political and strategic consequences for the Japanese government. Although Takaichi remains popular, rising prices have cut into her poll numbers. Market jitters are already fueling intra-party grumbling over her expansionary fiscal stance, which envisions a sharp reduction in the national consumption tax and large public investment into AI, fusion, quantum, and other sectors to support ambitious economic and technology goals. A prolonged crisis would squeeze these investments and limit Tokyo’s ability to increase defense spending, undermining shared economic security goals at a moment when Japan’s relations with China are at a low point.

- Japan’s naphtha crunch exposed a blind spot for the global economy: disruption of petroleum byproducts. While governments have spent decades stockpiling crude and diversifying energy supplies, few had accounted for disruptions to the refined byproducts that quietly underpin modern manufacturing — such as naphtha, a key feedstock in the production of plastics, chemicals, and synthetics used across a wide range of industries and consumer goods sectors. With no strategic reserve and 70 percent of its supply sourced from the Gulf, Japan watched naphtha shortages cascade through supply chains in ways that crude reserves could not offset — disrupting production of everything from medical devices to auto parts.

For decades, Japan believed it was well prepared for energy crises, backed by robust crude oil stockpiles and well-diversified LNG supplies. But there were blind spots: it relied on the Gulf producers for more than 90 percent of its crude imports and for a majority of its naphtha needs that exposed critical sectors — from construction and healthcare to auto manufacturing — to risks of supply disruptions in the region.

Pre-War Snapshot

Japan’s Annual Commodity Imports from the Gulf, 2025

Economic Impacts

Macroeconomic Picture

Higher energy, shipping, and input costs are weighing on GDP growth, with the Bank of Japan halving its forecast to 0.5 percent for FY2026. Naphtha’s broad manufacturing uses mean that “Hormuz inflation” is propagating through household budgets three times faster than a conventional energy shock, disrupting production of automobiles, home construction, and thousands of consumer products. Dollar-denominated import payments are meanwhile weakening the yen and compounding import costs. Together, accelerating inflation and softening growth leave the Takaichi government navigating a stagflation risk that will grow if disruptions persist.

Petrochemicals

Japan’s petrochemical sector — the world’s fourth largest and 12 percent of manufacturing output — converts Gulf-sourced crude and naphtha into the plastics and synthetics that underpin Japan’s industrial base. Distinct from China, Japan sources both upstream crude and downstream intermediates from the Gulf, exposing every production stage simultaneously. That structural vulnerability is now translating into measurable damage: Mitsui Chemicals has absorbed a USD 100 million operating hit tied to the conflict, while Mitsubishi Chemical Group is weighing a breakup of its petrochemicals unit. Although naphtha shortages are expected to ease by end-2026, constrained feedstock supply is surfacing competitiveness pressures across Japan’s manufacturing sector that have few short-term domestic fixes.

Japan sources both upstream crude and downstream intermediates from the Gulf, exposing every production stage simultaneously.

Automotives

The auto sector — Japan’s main economic engine, comprising nearly 3 percent of GDP and 14 percent of manufacturing output — was already under stress from U.S. tariffs, Chinese competition, and a stuttering EV transition before Hormuz disruptions compounded the shock. Roughly 70 percent of Japan’s aluminum and naphtha, used in auto parts such as such as bumpers and door panels, is sourced from the Gulf. Disruptions to both materials are driving production cuts and delays: Toyota projects a reduction of over 80,000 vehicles through November, with Honda, Subaru, Nissan, and Mitsubishi also forecasting profit hits. Higher energy prices are simultaneously pushing up operating costs, suppressing domestic demand, and accelerating the global EV transition — where Japanese carmakers are far behind Chinese rivals.

Japan: Risks & Opportunities by Sector

Outlook

Japan can manage continued disruptions for now: stockpiles can absorb further supply shocks, energy subsidies are funded through the fall, and U.S. naphtha imports have restored supply to roughly 80 percent of pre-crisis levels. Politically, Takaichi has breathing room. Japanese voters are dissatisfied with the government’s inflation and financial countermeasures but so far do not blame her for the crisis. Her approval ratings, while down from historic highs in early 2026, remain at well over 50 percent.

With debt servicing already consuming 25 percent of Japan’s budget, new relief measures would add fiscal stress.

But if energy and supply shocks continue to compound through the end of the year, inflation will likely balloon, forcing Takaichi to make difficult trade-offs. With debt servicing already consuming 25 percent of the budget, new relief measures would add fiscal stress. Even prior to the emergency spending measures to respond to the Hormuz disruptions, economics and business leaders were questioning Takaichi’s aggressive economic and defense spending plans. Markets are sending government bond yields to three-decade highs, and the economic impacts of the Iran war will likely lead to less ambitious spending increases. If fiscal pressures continue to mount, public dissatisfaction and internal LDP dissent will likely grow, jeopardizing Takaichi’s broader governing and legislative agenda — including constitutional revision, security policy reforms, and defense modernization — that have geopolitical consequences.