Southeast Asia

- Southeast Asia’s emerging economies are coping so far but face growing fiscal and cost-of-living challenges. The region’s emerging markets lacked the commodity reserves, fiscal headroom, and financial strength that Asia’s advanced economies enjoyed at the outset of the conflict, and the economic impacts have been more rapid and painful. Fuel subsidy systems have cushioned effects on consumers so far but are straining amid a disruption of this duration and magnitude.

- Inflation could have near-term political consequences in key markets. Rising energy prices are flowing into higher costs for manufacturing, logistics, and construction across the region. Cost-of-living pressures are becoming politically visible. In Vietnam, fuel shortages and panic buying resulted in queues at petrol stations in major cities in March. Spiking inflation and economic pressures have led to labor strikes and are deepening political divides in the Philippines. In Malaysia, Prime Minister Anwar Ibrahim is reportedly considering calling snap national elections one year earlier than expected to renew his mandate ahead of politically toxic but fiscally necessary subsidy reforms exacerbated by disruptions in the Strait of Hormuz.

- The crisis complicates — but does not derail — the region’s future as a low-cost advanced manufacturing and technology hub. Before the conflict, Southeast Asia was on a strong trajectory in moving up the manufacturing and technology value chain: it attracted USD 235 billion in foreign direct investment (FDI) in 2024, outpacing China as multinationals diversified supply chains. But the crisis has exposed the region’s relative energy dependence as a key vulnerability for its competitiveness and attractiveness as an FDI destination. At the same time, the conflict could create opportunities as AI companies exposed in the Middle East could look to Malaysia and other regional markets as alternatives. The countries that can most quickly diversify energy sources, including by pivoting to nuclear or renewables, will be poised to benefit.

- Southeast Asia’s governments are recalibrating the balance between Washington and Beijing. As the economic fallout from the conflict deepens, public opinion across Asia is blaming the United States, giving governments political as well as economic reasons to hedge toward Beijing. Few will align fully with China, but the drive to diversify will lead to deeper partnerships across multiple fronts: with regional middle powers, Europe, and China itself.

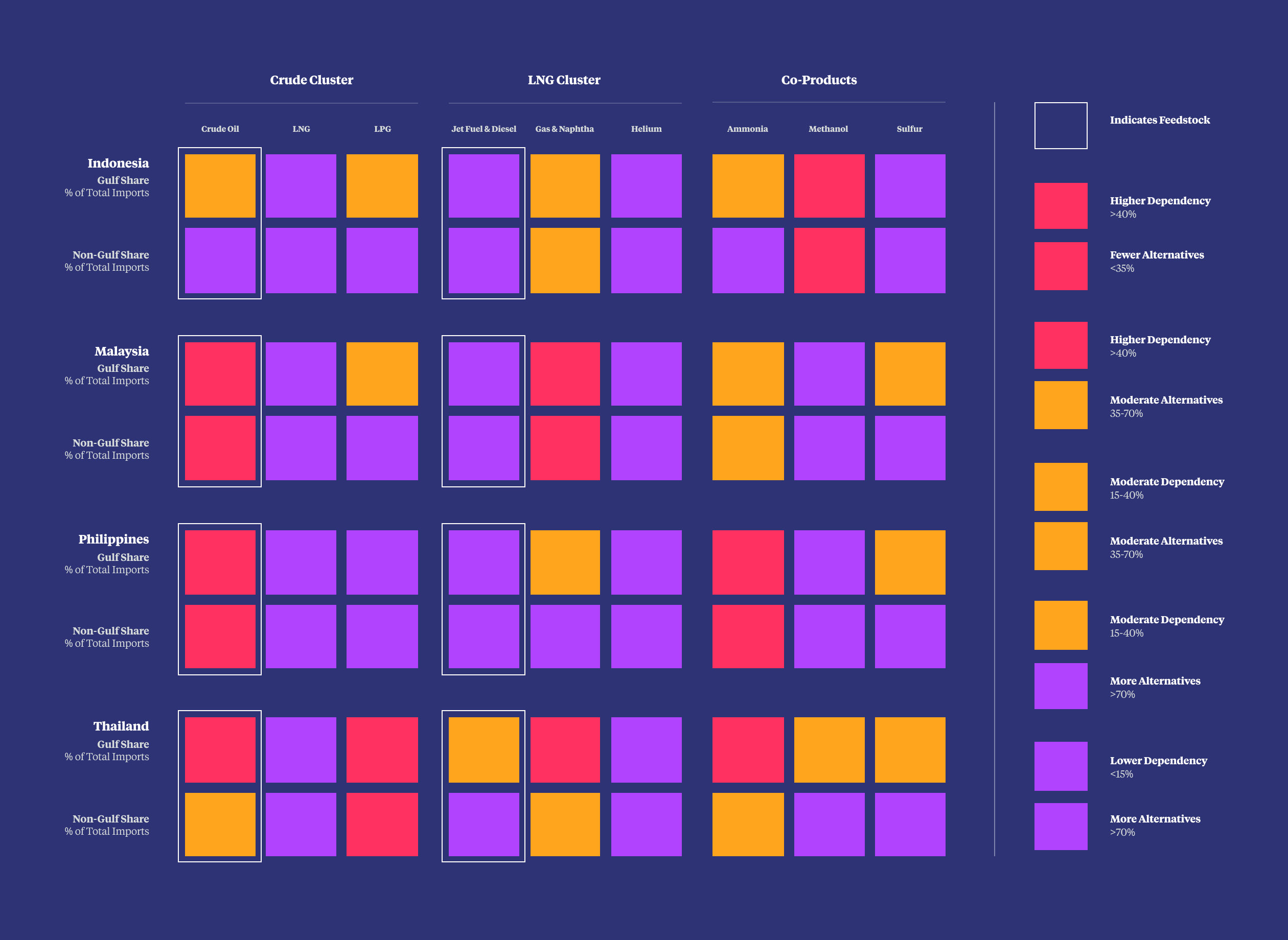

Prior to the crisis at the Strait of Hormuz, most Southeast Asian markets relied on the Gulf for much of their oil supply, with LNG more diversified but still dependent on the Middle East.

Pre-War Annual Gulf Imports vs. Alternative Imports, 2025

Key Takeaways by Market

Pre-War Annual Absolute Gulf Commodity Imports by Economy, 2025 (Metric Tons, Rounded)

Indonesia

Indonesia has moved rapidly to diversify energy sources, but the Hormuz crisis exposed its vulnerability as a net energy importer with a budget anchored to commodity prices it cannot control. Through subsidies and price caps, Jakarta is effectively absorbing oil price shocks of up to USD 100 per barrel. With the fiscal damage for 2026 largely locked in, the crisis is amplifying preexisting concerns around a weak tax base, rising spending commitments, and fiscal sustainability that have rattled investor confidence.

Vietnam

Vietnam has fast-tracked the establishment of a strategic petroleum reserve, lowered import tariffs on fuel products, and diversified crude supplies, but has limited room to absorb a prolonged disruption. The combination of rising inflation and U.S. tariff pressure will challenge double-digit growth targets and undermine investments in energy-intensive sectors such as data centers, semiconductors, AI, and advanced manufacturing.

Thailand

Thailand entered the crisis with lackluster domestic demand and modest growth rates that lagged its regional peers. While the crisis alone is unlikely to create major political instability, it contributes to broader public dissatisfaction amid weak growth, high household debt, and rising consumer prices.

Malaysia

Malaysia is comparatively insulated as a net oil exporter, but its refining and downstream petrochemicals sectors are hit by rising LNG costs and crude supply disturbances. Malaysia faces unsustainable fuel subsidy bills even as Petronas, the national oil company, benefits from elevated export revenues.

The Philippines

The Philippines imported over 95 percent of its crude from the Middle East prior to the conflict and is highly exposed to disruptions in remittances from Gulf-based overseas foreign workers, whose income is crucial to the country’s consumption-driven economy. Philippine President Ferdinand Marcos declared a national energy emergency in March as the impact of fuel prices surged across transport, food, and utilities. Increased inflation and fiscal pressures are deepening the country’s political fissures.

Economic Impacts

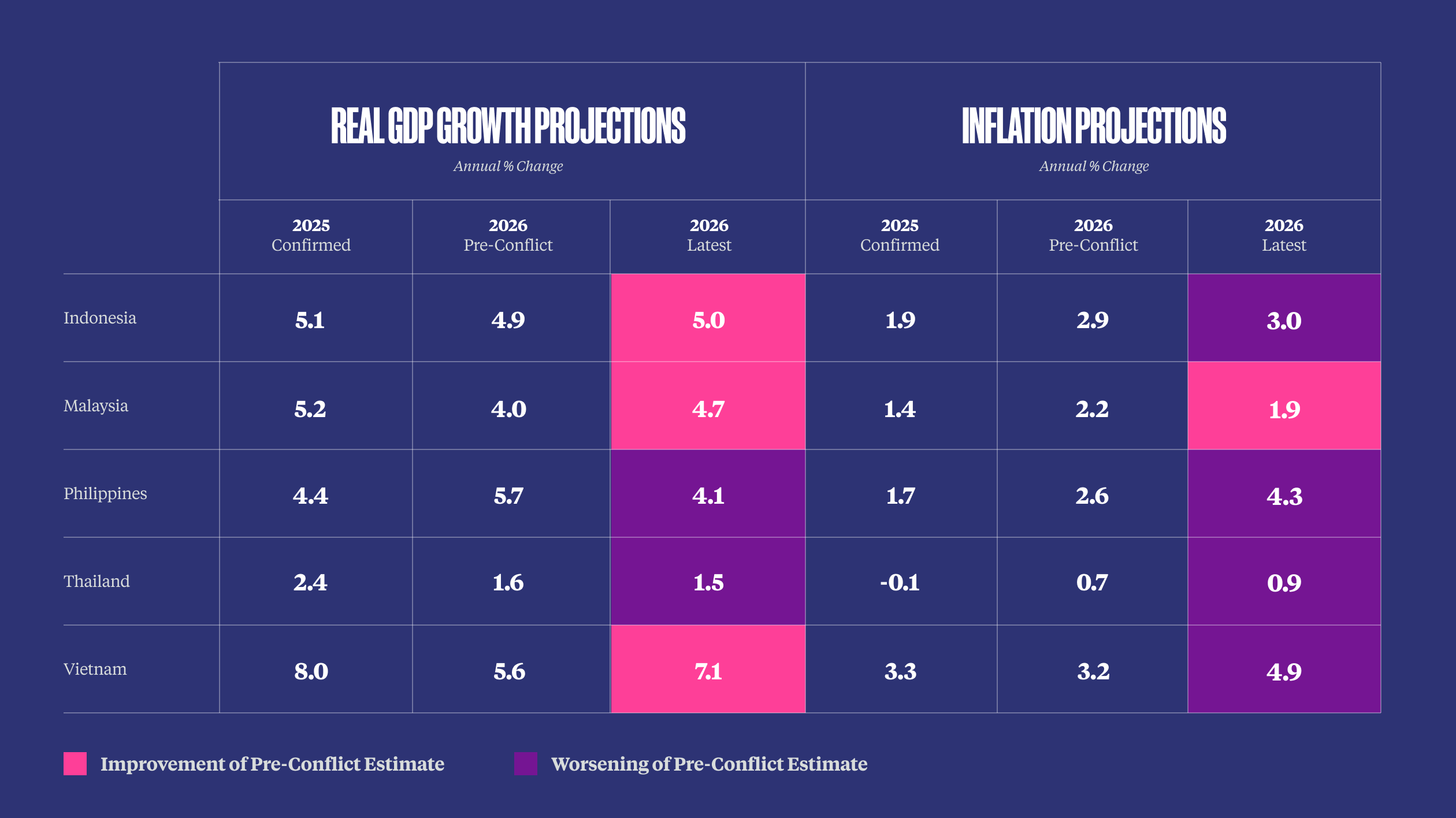

The region’s growth outlook is dimming and inflation is rising. Growth forecasts across the region have been revised downward and higher energy costs are hitting consumers through fuel, food, and utilities prices. In the Philippines, consumers are increasingly turning to credit cards and short-term lenders to alleviate financial stress and meet basic needs. Food inflation is approaching 5 percent in Indonesia.

Fiscal pressures are mounting across the board. Governments have deployed subsidy extensions, emergency borrowing, and targeted relief to manage fallout from Strait disruptions. Thailand approved a USD 12.2 billion emergency borrowing package; the Philippines has released USD 350 million in fuel and transport subsidies; and Indonesia has committed USD 14 billion to freeze fuel and LPG prices through the end of 2026. Vietnam has kept domestic petrol prices in check through tariff cuts on petroleum products and a fuel price stabilization fund, though the latter is quickly drawing down. Malaysia’s fuel subsidy bill has increased tenfold, creating acute fiscal pressure. Across all five markets, the central fiscal question is how long these interventions can be sustained without triggering a loss of investor confidence or crowding out other spending priorities.

Spotlight on food security

Southeast Asia’s agricultural sector, dominated by rice production, is acutely exposed to disruptions in the supply of key fertilizer inputs: in particular, urea, for which the region depends heavily on Qatari and Saudi exports, and sulfur, a byproduct of Gulf refining with few viable alternative sources at scale. Ammonia exposure varies significantly given domestic production capacity in Indonesia and Malaysia.

The region’s rice growers are predominantly smallholder farmers operating on thin margins, and rising fertilizer costs are coinciding with a period of relatively low food prices, creating a damaging squeeze from both ends. In response, farmers are reducing fertilizer application, switching to less input-intensive crops, or foregoing the summer planting season altogether. The effect on food prices has so far been gradual, but the consequences for the fall harvest are already baked in. They will also intensify if the moderate El Niño event currently forecasted disrupts monsoon rainfall, as occurred in Vietnam and Thailand in 2015-16, when the region experienced its worst drought in two decades.

Rising fertilizer costs are coinciding with a period of relatively low food prices, creating a damaging squeeze from both ends for smallholder farmers operating on thin margins.

The global price contagion risk is concentrated in Thailand and Vietnam, which together account for the bulk of the region’s rice exports. The domestic food security risk is most acute in Indonesia and the Philippines, net-importing countries where production shortfalls cannot be offset by reduced exports. While policy buffers may absorb some of the shortfall, the aftereffects of current supply disruptions could start to appear in headline food prices within 60-90 days and reverberate over the medium term.

Sectors to Watch

Manufacturing

Higher energy and petrochemical prices are raising production costs for steel, chemicals, electronics, footwear, apparel, and other goods across Southeast Asia’s export-driven economies. Given the region’s outsized dependence on imported fuel, a prolonged period of higher energy prices could erode the manufacturing competitiveness that underpins foreign investment and the “China Plus One” diversification strategies multinationals have pursued as a tariff hedge. The risk in most markets is not an immediate production shock but a gradual erosion of profitability, competitiveness, and investment sentiment.

Metals

Indonesia’s nickel industry sourced roughly 75 percent of its sulfur — used to make the sulfuric acid that is essential to minerals and metals refining and processing — from the Middle East prior to the conflict. Sulfur prices have roughly doubled since the March and now account for a significant portion of nickel processing costs. Several of Indonesia’s major nickel processors have cut output by as much as 10 percent. Higher diesel and chemical processing costs could also weigh more broadly on Indonesia’s copper, tin, gold, and coal mining industries.

Technology & IT

Across the region, the semiconductor and electronics industries face higher energy costs and supply chain disruptions, and local chip producers are less able to absorb higher input costs — such as for helium — than the most advanced and well resourced semiconductor firms in the United States, Taiwan, and Korea. Malaysia’s rapidly growing data center industry is also being squeezed by higher power and cooling costs, threatening the economics of an AI infrastructure buildout that has been a central draw for foreign investment. In Vietnam, rising costs complicate Hanoi’s plans to expand into energy-intensive sectors such as data centers, semiconductors, AI, and advanced manufacturing. In the Philippines, elevated utility costs are disproportionately hitting the business process outsourcing sector, a key GDP contributor and major employer. Higher input and logistics costs for the electronics and hard-disk-drive assembly industries complicates Thailand’s positioning as a regional manufacturing hub.

Aviation & Tourism

Jet fuel price increases, higher airfares, and flight route reductions are hitting tourism-dependent economies across the region. Bali has seen a steep drop in travel from the Gulf and Europe, and Thailand faces disruption to key Gulf aviation transit corridors. The impact is broadest in Indonesia, where air travel is often the only practical option for long-distance domestic movement across the archipelago.

Political Impacts

Cost-of-living pressure is the main economic risk across the region’s politics. Governments have absorbed much of the shock to date, but fiscal space is diminishing and the tension between fiscal sustainability and political stability remains unresolved.

Malaysia faces the most immediate political fallout as rising inflation and sharply increased fuel subsidy bills raise pressure on Prime Minister Ibrahim to adopt fiscally necessary but politically unpopular reforms. While Anwar remains favored to win reelection, the crisis is deepening instability within his already fractious ruling coalition, and election dynamics will slow decision-making and heighten political risk.

In Indonesia, the memory of the August 2025 protests — the largest public backlash of President Prabowo’s first year — has reinforced extreme caution about price adjustments. That Prabowo is reportedly weighing adjustments to his flagship free-lunch program underscores the extent of fiscal pressures.

In the Philippines, the crisis has sharpened the political feud between factions aligned with President Marcos and Vice President Sara Duterte, with the Duterte-aligned opposition capitalizing on cost-of-living anger. With an estimated 1.1 million Filipino workers employed across the Middle East, pressure on this important financial lifeline for many middle-class and low-income families could trigger further unrest in a highly politicized environment.

Outlook

Continued disruptions to Strait transit could generate economic, fiscal, and political inflection points across Southeast Asia’s emerging markets in the near term. Indonesia faces a budget deficit revision this summer that could breach the legal 3 percent of GDP threshold, with implications for investor sentiment. Vietnam must decide whether to hold fuel prices below cost or accept a politically difficult adjustment. Thailand’s inflation trajectory towards a projected 5.2 percent peak will test government relief measures and monetary policy flexibility. The Philippines faces compounding pressure from inflation, peso weakness, and political dysfunction. Malaysia’s subsidy bill is unsustainable at current levels, and the government will need to signal a credible reform path even if implementation is deferred.

Continued disruptions to Strait transit could generate economic, fiscal, and political inflection points across Southeast Asia’s emerging markets in the near term.

If disruptions persist through late 2026, the challenge shifts from stabilization to managing sustained stagflationary pressure, with deeper growth downgrades, thinning fiscal buffers, and harder tradeoffs between inflation control, social support, and investor confidence.

The most consequential medium-term effect, however, may be structural: across all five markets, the crisis is accelerating the political and commercial case for renewable and nuclear energy, LNG supply diversification, investment in domestic energy production, and grid modernization. A disruption that began as a supply shock is reshaping the region’s long-term energy investment priorities and potentially accelerating a consequential market shift.