India

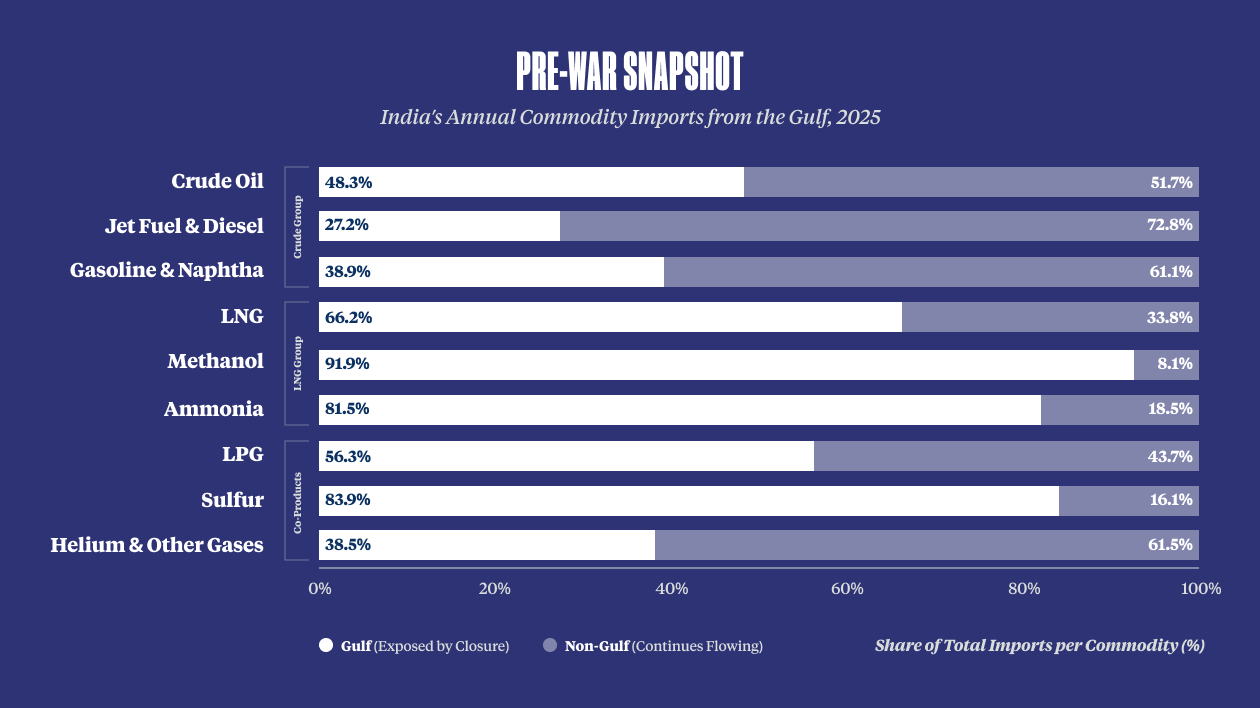

- India faces continued, compounding exposure from Hormuz disruptions. Before the conflict, over 40 percent of India’s crude imports, and roughly 60 percent of liquid natural gas (LNG) and liquid petroleum gas (LPG) imports (the latter used for cooking and heating), transited the Strait. Supply shocks for fertilizers and petrochemical manufacturing inputs, elevated freight costs, and reduced remittances from Indian workers in the Gulf create a much broader transmission channel across the Indian economy than a conventional oil-price spike alone.

- A convergence of fuel, food, and agricultural shocks could create cost-of-living challenges and enhance political concerns. Food and fuel together account for over half of India’s consumer price basket, and higher fuel costs are already hitting households even though New Delhi has absorbed some of the incremental costs. Disruptions in fertilizer supplies are worrying farmers and agro-economists, just as forecasts indicate a below-normal monsoon season.

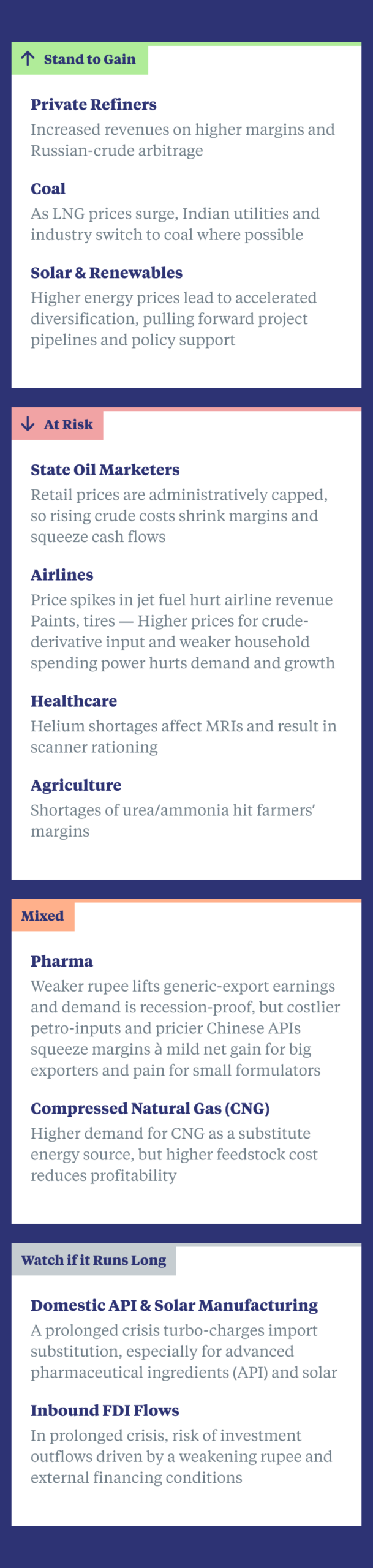

- Pressure on India’s pharmaceutical sector has global consequences. Higher energy, petrochemical, and imported input costs pose challenges to one of India’s most globally competitive industries. India is the world’s leading supplier of generic medicines and vaccines by volume, so any resulting production cuts could impact drug availability and healthcare provision globally.

- India’s buffers are real but time limited. Domestic consumption has historically insulated India from external shocks better than most peers, but prolonged disruptions will erode that cushion.

India is the world’s third-largest importer of oil, fourth-largest of liquid natural gas (LNG), and second-largest of liquid petroleum gas (LPG). Before the closure of the Strait of Hormuz, India sourced significant portions of these commodities from the Gulf, relying on their transit through the Strait. It also depended on inputs that transited the Strait as feedstock for its key exports, ranging from refined petroleum and petrochemical exports, as well as medications and pharmaceuticals.

Pre-War Snapshot

India’s Annual Commodity Imports from the Gulf, 2025

Economic Impacts

Macroeconomic Picture

Government interventions such as subsidies and fuel tax cuts are mitigating the impacts so far, but at growing fiscal cost. Households are already feeling the strain: the administered price of cooking gas cylinders has been raised twice, and subsidized refills for low-income families have been cut. A sustained Hormuz disruption would not derail India’s growth ambitions, but it could fuel inflation, widen India’s current account deficit, and weaken the Indian rupee, all of which could crowd out private investment over time.

Agriculture & Food Security

Price increases from prolonged LPG disruptions, which over 60 percent of Indian households rely on for cooking, would show up quickly in household budgets and public sentiment. India sources nearly 84 percent of sulfur imports from the Gulf, leading to higher fertilizer costs. With 42 percent of India’s workforce employed in agriculture, even a moderate shock to farm economics would have outsized consequences for rural consumption and employment.

Over 60% of Indian households rely on LPG for cooking – and prices have already gone up twice.

Pharmaceuticals

India’s generic pharmaceutical sector operates on very thin margins, and its global competitiveness depends on affordable energy, reliable petrochemical inputs, and access to imported raw materials. Prolonged Hormuz disruptions would affect all three. Higher oil and petrochemical prices would increase domestic manufacturing and packaging costs. Imported active pharmaceutical ingredients (APIs) and intermediates would become more expensive. Higher freight, insurance, and fuel costs would further compress margins. The result is a challenge for one of India’s most visible and strategically important export sectors, although India’s largest pharmaceutical players may be better able to absorb the margin pressure and gain market share.

Renewables

If energy prices stay high, India’s energy transition will likely experience faster and more urgent deployment even as supply chain dependencies threaten to cap its pace. Already, India added a record 55 gigawatts (GW) of non-fossil fuel capacity in 2025, with its EV market projected to grow from USD 2 billion today to USD 164 billion by 2033. The durability of India’s production-linked incentive schemes, which offer manufacturers financial incentives tied to incremental domestic output rather than up-front subsidies, will be an important predictor of New Delhi’s ability to build a domestic clean-tech manufacturing base. However, China’s rare earths dominance means India risks replacing one import dependency with another; India is attempting to navigate this challenge with domestic investments and international partnerships.

India: Risks & Opportunities by Sector

Outlook

Compounding cost-of-living pressures are the main vector by which commodity disruptions could become a deeper economic and political challenge for the Indian government. New Delhi has deployed tools, including subsidies, fuel tax cuts, and targeted welfare programs, to cushion the short-term impacts, but sustained intervention would strain public finances and complicate efforts to maintain budget discipline.

Sustained government intervention would strain public finances and complicate efforts to maintain budget discipline.

LPG availability, fertilizer prices, freight costs, and monsoon performance are key indicators to watch to determine whether disruptions are compounding to create a wider inflationary challenge. Government decisions on whether to extend subsidies and tax relief measures will be important signals of New Delhi’s concern. Sustained pressure on rural incomes and manufacturing margins could also erode public support for trade liberalization even as India is negotiating and benefiting from greater economic integration with a range of global partners, including the United States, which has emerged as a key source of LPG since the start of the crisis.

For India’s energy mix, continuing disruptions could accelerate trends already underway, including a push to diversify energy suppliers across geographies as diverse as Russia, Africa, and North and South America. They could also fast-track domestic efforts to expand domestic energy supply in ways that reshape India’s energy posture for the longer term. New Delhi could open up for development areas with proven energy reserves such as in India’s northeastern states, pave the way for companies to explore for gas deposits in the Andaman Sea, and introduce incentives for coal gasification.